Every family, looking at the next generation, hopes to confer advantages that are more than just material and financial – inculcate character and leadership, to inspire creativity and enterprise, to help all family members find and follow their individual callings, and to avoid the financial dependency and loss of initiative that can all too often be an unwanted consequence of financial success. Yet many families never succeed in realizing that vision, much less sustaining it for three, four, or five generations and beyond.

James Hughes from his book Family Wealth: Keeping It in the Family

When considering planning for future generations, every family has a unique set of values, priorities, and circumstances which call for bespoke plans incorporating professional advisors across multiple disciplines: legal and tax advisory, investment brokerage, and insurance professionals all take a seat at the table as families consider the pros and cons of strategies.

ThorCo Solutions, LLC and its network of professional affiliates have a long history of serving families with objectives including the transfers of closely-held business interests and real assets across multiple generations while contemplating family dynamics, practical constraints, preference to minimize taxation, and support certain philanthropic causes.

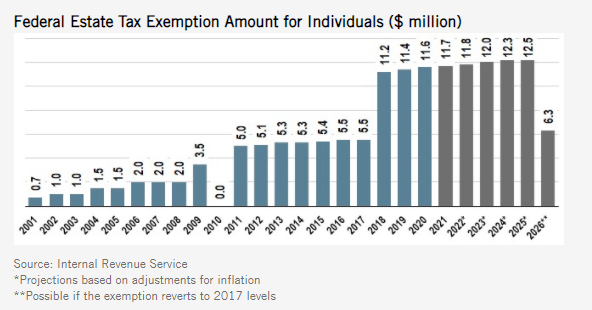

First, though, a reminder that the exemption amount, per individual, for the Federal estate tax is presently historically high. In 2022 the indexed exemption is $12,060,000 per person. It is scheduled to decrease to 2017 (indexed) levels in 2026. The Federal estate tax rate is roughly 40%.

Importantly, many states also include an estate or inheritance tax. For example, Connecticut has an estate tax rate of of 10.8-12% with an exemption amount of a bit more than $7,000,000. New York has an estate tax rate of 3.06-16% with an exemption amount of $5,930,000.

Pennsylvania and New Jersey, in contrast, have no estate tax. They both have an inheritance tax, though, which does not apply to the estate but, rather, the individual receiving the inheritance. According to Kiplinger, for New Jersey, “[n]o tax is imposed on transfers to the decedent’s spouse, domestic partner, parents, grandparents, children and their descendants, or step-children (step-grandchild and their descendants are not exempt). The first $25,000 of property inherited by a decedent’s sibling, son-in-law or daughter-in-law is also exempt. After that, they must pay the inheritance tax at rates ranging from 11% to 16%. All other individual heirs pay a 15% tax on the first $700,000 of inherited property and a 16% tax on everything over $700,000.”

Pennsylvania, also according to Kiplinger, “…has an inheritance tax, but it doesn’t apply to property inherited by the decedent’s spouse, parents (if the decedent is age 21 or younger), or child age 21 or younger. The tax is imposed at a 4.5% rate for the decedent’s parents (except if the decedent is 21 years old or younger), grandparents, lineal descendants, son-in-law, or daughter-in-law. The rate is 12% for people who inherit property from a sibling and 15% for all other heirs. A 5% discount is allowed if the tax is paid within three months of the decedent’s death.”

So what tools are used by families to plan for taxes and transfers? While there is no single answer, the following list of strategies is typically evaluated:

- Review of asset ownership and gift strategies, including use of the 2022 exclusion amount of $16k per individual per beneficiary per year for Federal purposes.

- Review of insurance policy ownership and consider use of an Irrevocable Life Insurance Trust (ILIT) with Crummey provisions. Keep in mind that, while life insurance proceeds are generally not taxable as ordinary income to beneficiaries, it may be includable in the gross estate for estate tax purposes. The use of a proper ILIT should cause death benefits to avoid estate taxation.

- Consider use of a premium-finance facility for payment of insurance premiums. The family office professionals at Momentum Advanced Planning have written some nice white papers on this strategy, including this article.

There are hosts of strategies including the sale of assets into Intentionally Defective Grantor Trusts (IDGT), Family Limited Partnerships (FLP), and Intergenerational Split Dollar which may be very helpful to certain families. We have also implemented Charitable Remainder Trusts (CRT) and Charitable Lead Trusts (CLT) in past years. In each case, the mechanism needs to be understood for implications to current and future tax liabilities, control issues, and possible implications to the plan as a consequence of future tax reform, changes to the family structure, and/or modified priorities.

Most important, though, is to consider the goals and priorities of the family. One interesting case study is that of Warren Buffett, who has famously remarked that he wants to, “[l]eave the children enough so that they can do anything, but not enough that they can do nothing.”

I will close with some thoughts from James Hughes. (I highly recommend his book!)

Family wealth is not self-perpetuating. Without careful planning and stewardship, a hard-earned fortune can easily be dissipated within a generation or two. The phenomenon of the fleeting family fortune is so well recognized that it inspired a proverb: ‘Shirtsleeves to shirtsleeves in three generations.’

Families should employ multiple quantitative and, more importantly, qualitative techniques to enable them, over a long period of time, to make slightly more positive than negative decisions regarding the employment of their human, intellectual, and financial capital.

James Hughes from his book Family Wealth: Keeping It in the Family